Instrumental Variable (IV)

We will replicate the paper with economic models using Instrumental Variable (IV).

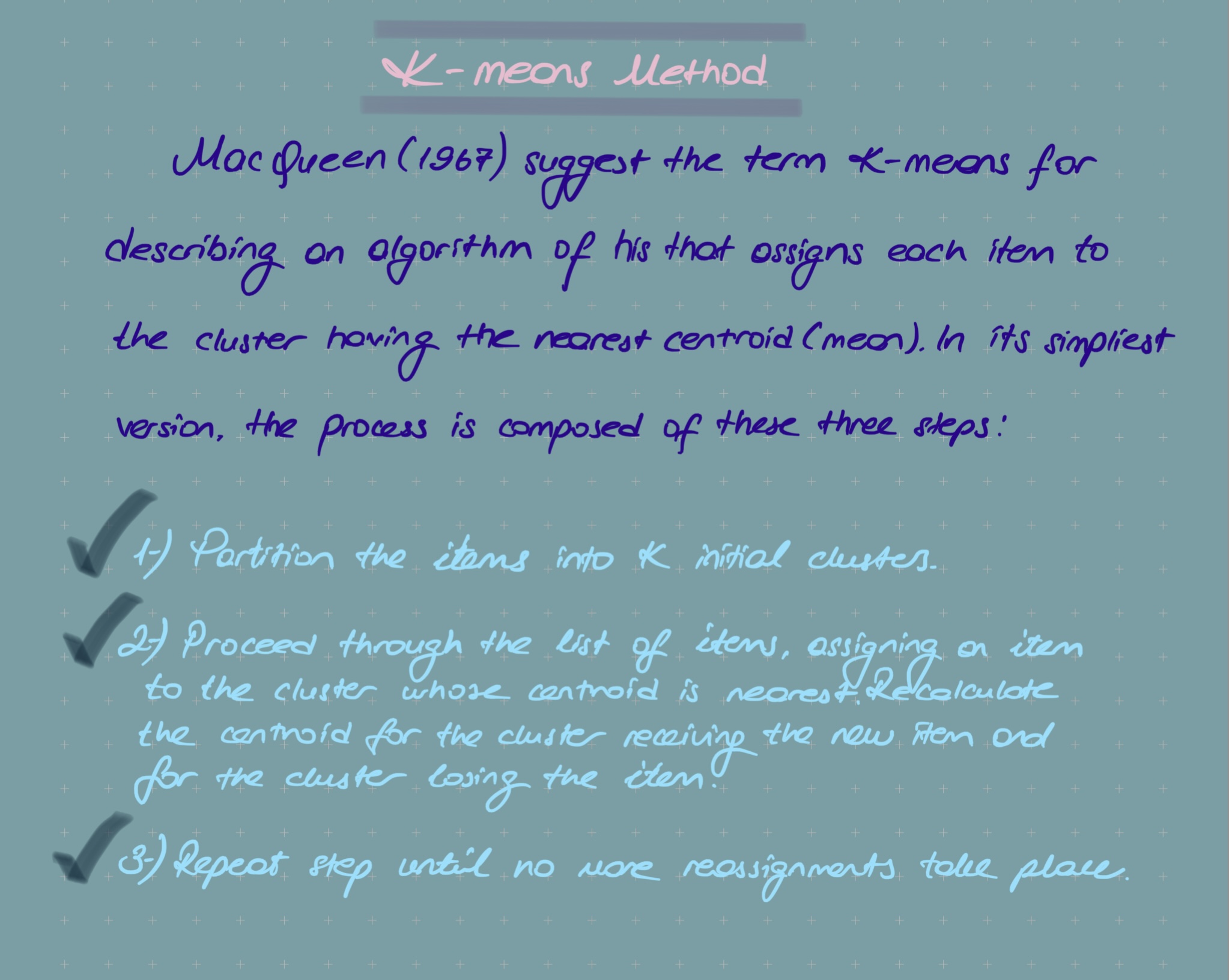

K-means Method - Finding the Best Clustering

We will create the best clustering using the k-means method.

Introduction to Econometrics: Linear Algebra

In this series, I will share both my theoretical and applied knowledge about econometrics. In this post, I will make important theoretical reminders about linear algebra.

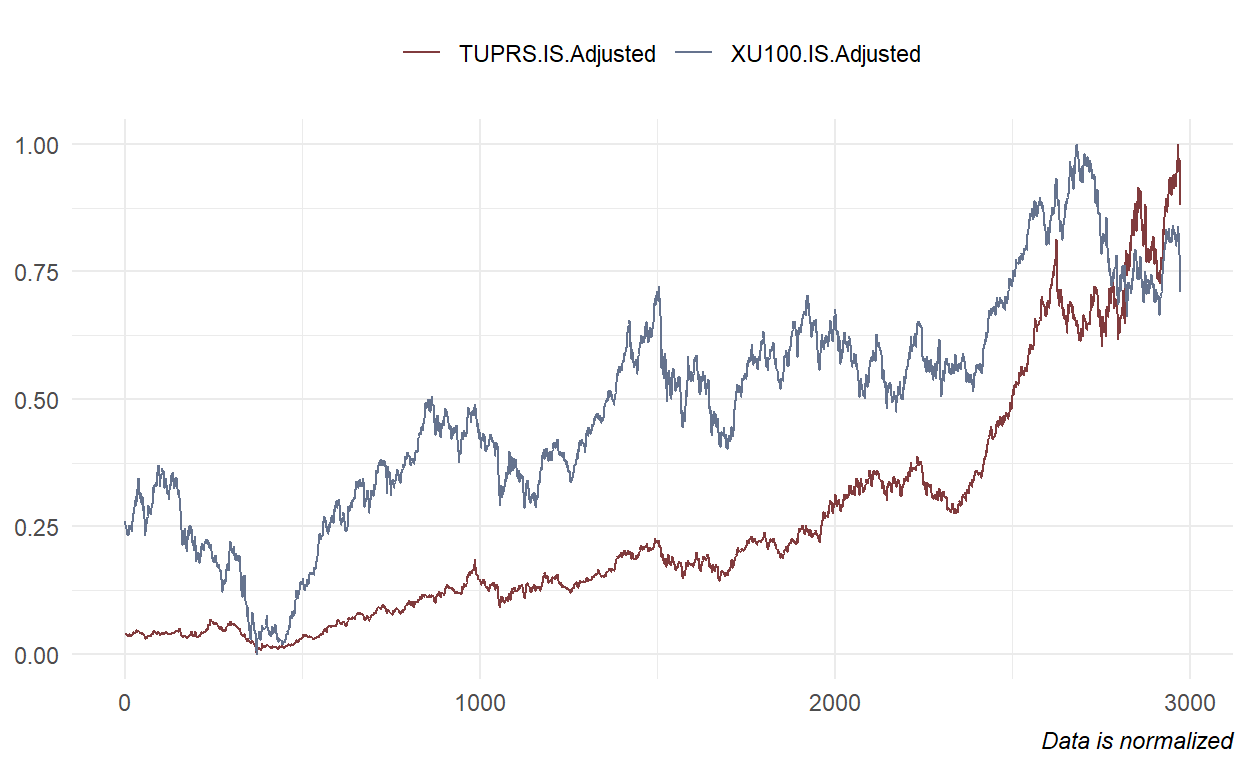

Equity Valuation Methods - Dividend Discount Model

I will evaluate using historical dividend data for TUPRS stock listed on Borsa Istanbul (BIST).

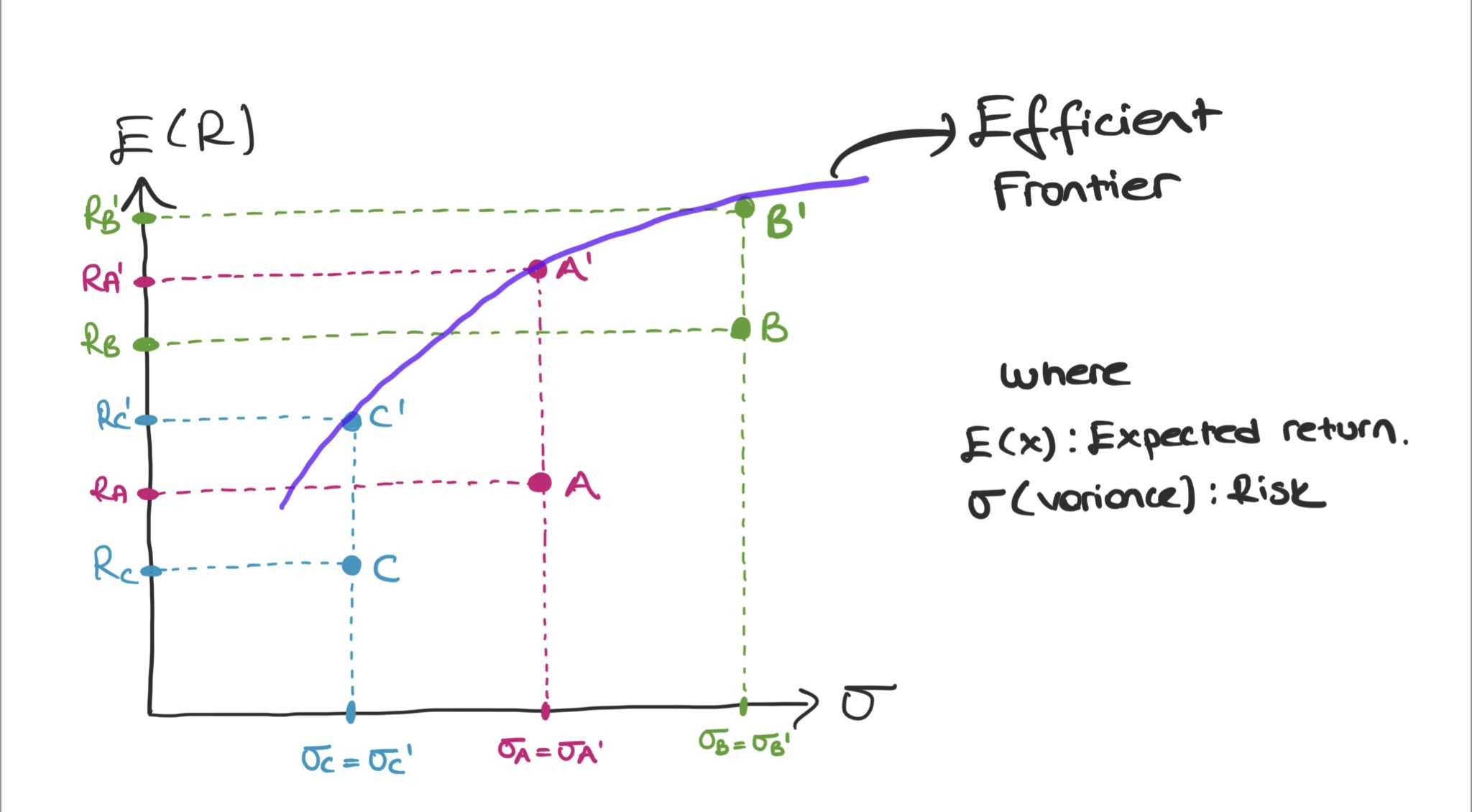

Portfolio Selection: Three Factor Model (Fama and French'93) vs Sharpe Ratio

In this study we will select a portfolio based on Fama and French's (1993) three-factor model study. Next, we will compare the sharpe ratio with the three factor model.

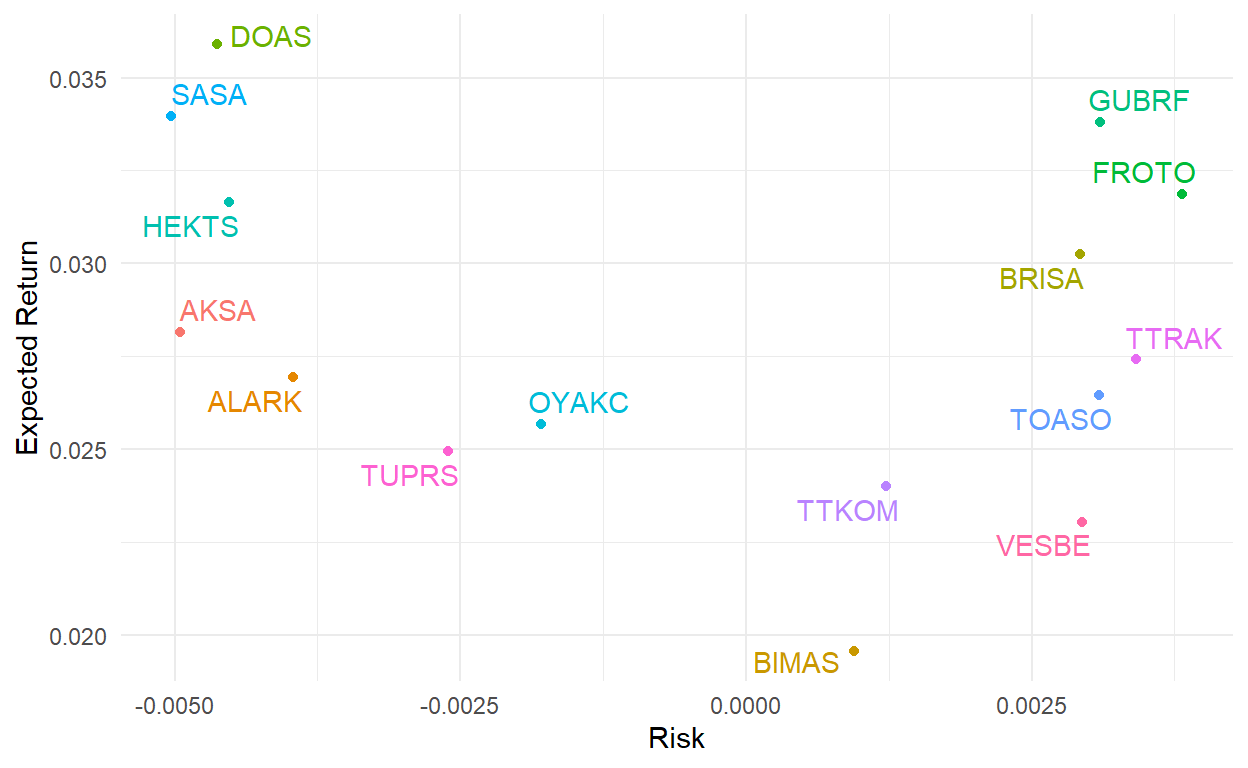

Optimum Portfolio Selection

We are gonna create the best portfolio with 10 stocks selected from BIST.

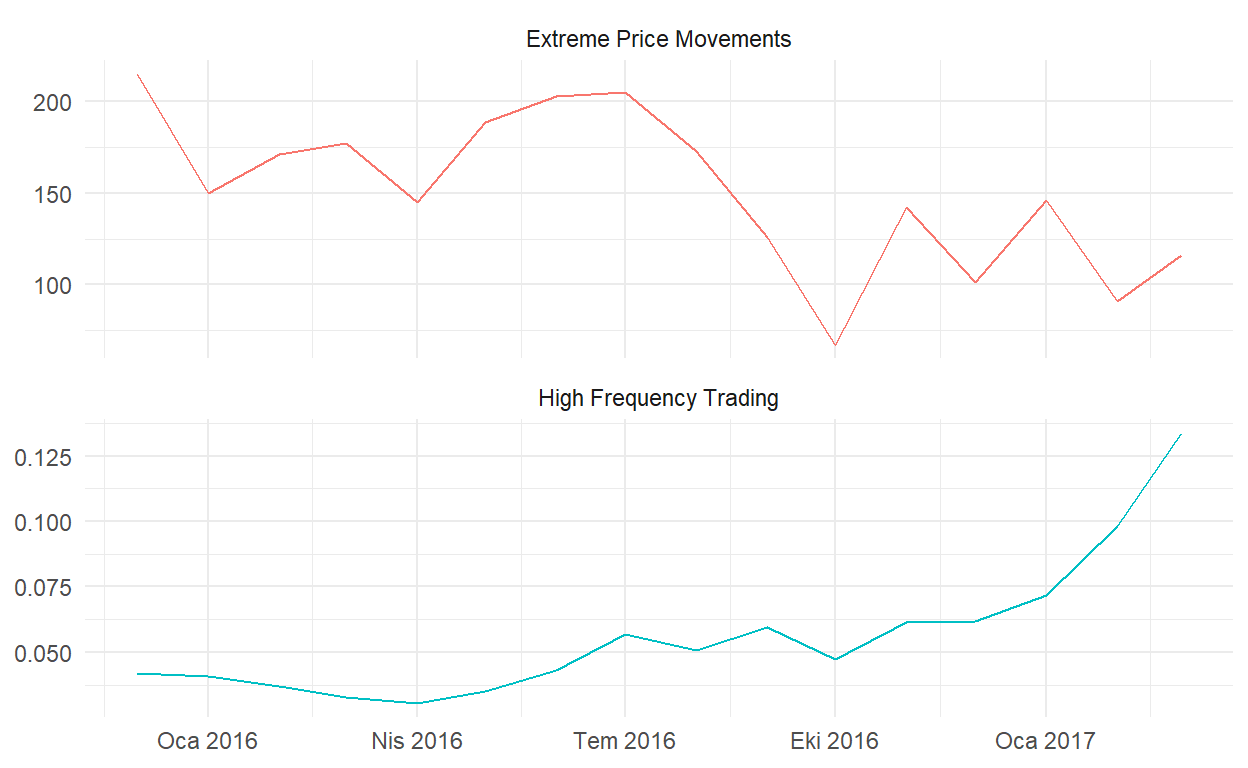

Investigating High-Frequency Trading (HFT) Around the Extreme Price Movements in Borsa Istanbul

In this study, I analyzed the existence of high-frequency trading (HFT) in Borsa Istanbul. My focus is it's the behavior and market share of high-frequency trading during extreme price movements (EPM).